{kind=link}

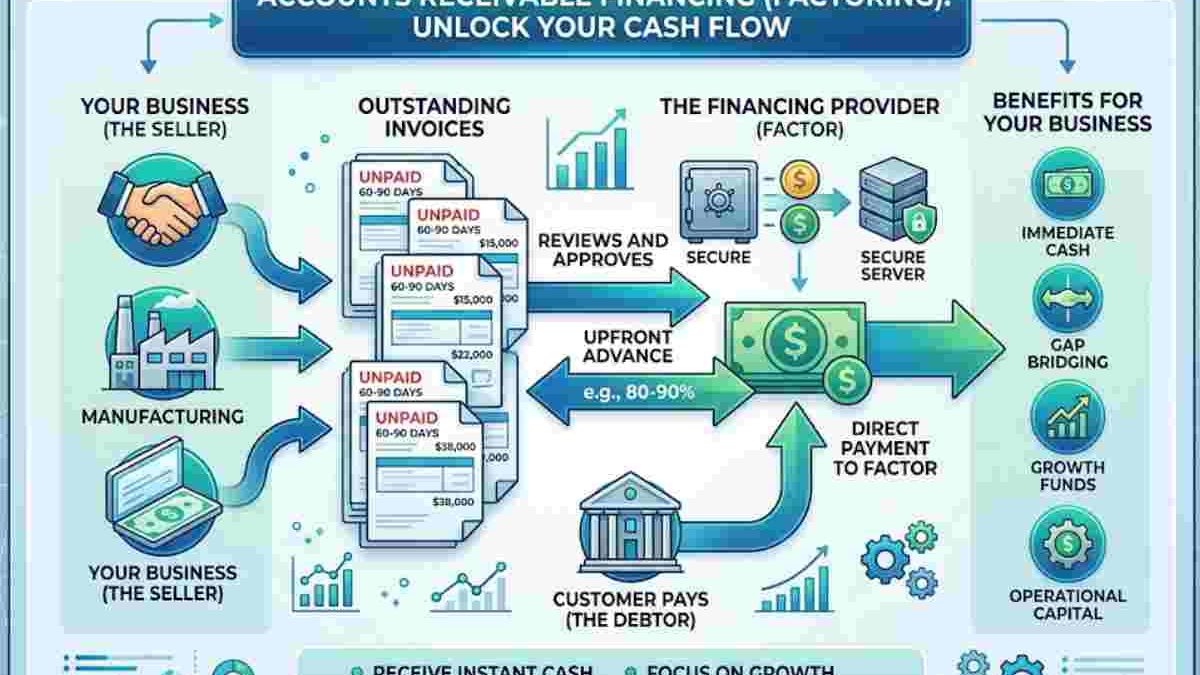

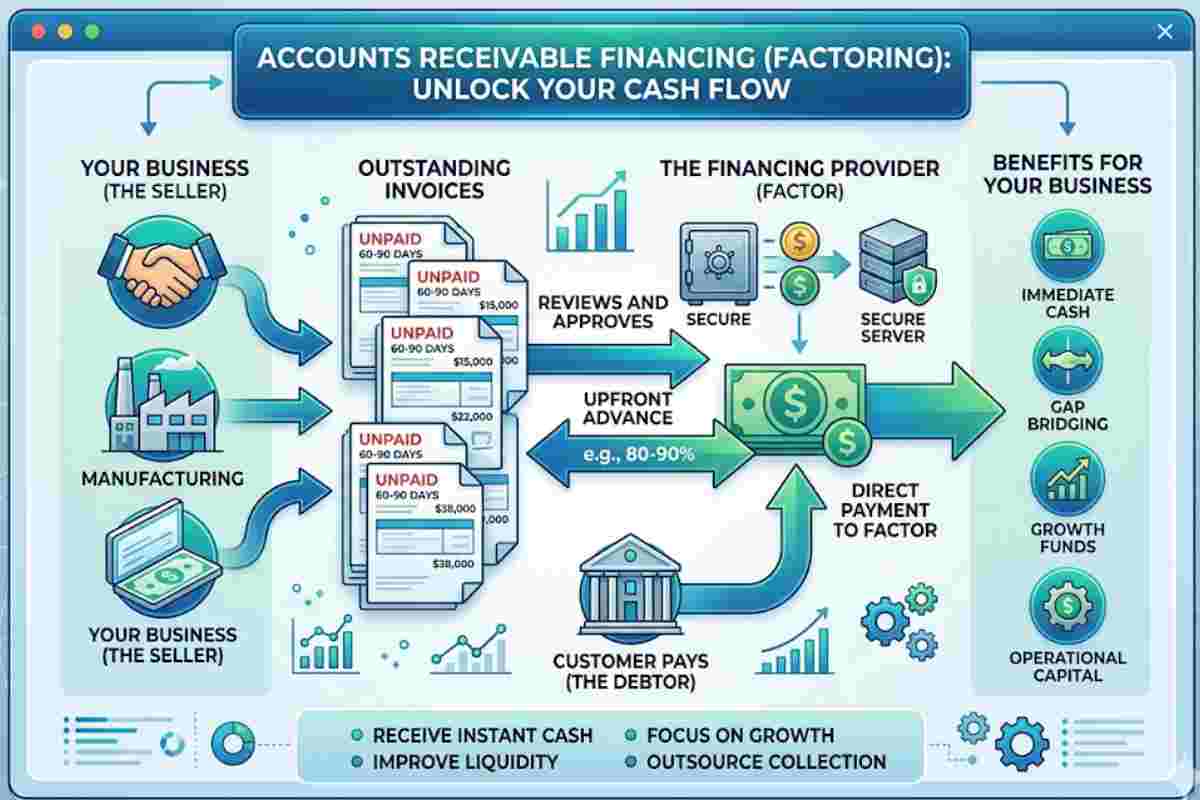

Accounts receivable financing is also known as factorization or accounts receivable financing. This process occurs when a business sells unpaid invoices (accounts receivable) to a third party like us. The third party (the “factor”) offers the company immediate cash, usually an agreed-upon percentage of the invoice amount. Once the invoice compensates, the remaining balance (less a commission) returns to the company.

Table of Contents

What Is Accounts Receivable Financing?

Many small and medium initiatives (SMEs) do not have the liquidity to purchase goods or raw materials to complete their export orders. However, foreign buyers require credit periods, which means that the business’s working capital will be limited to long-term invoices.

Accounts receivable financing is a short-term solution that helps businesses meet their financing needs before receiving payment from overseas buyers. Also known as invoice discounting, factoring, and factoring accounts receivable financing is Drip Capital’s solution for offering working capital to exporters.

How do Accounts Receivable Impact the Company’s Finances?

Finances have evolved remarkably in response to the scarcity of resources available to administrators to carry out company operations, with working capital being one of the most critical resources.

They must pay attention and seek to maximize its use, which is closely related to current assets and current liabilities, mainly cash, inventory, accounts payable, and receivable.

Accounts receivable are essential since they represent receivable assets for the company, rights with which it has to obtain aid for products or services brought. They are also crucial in upholding a healthy cash flow for its operations. Generally, the investment in accounts receivable represents a significant investment in the company since they represent claims of resources that transform into cash to complete the financial cycle in the short term.

Types of Accounts Receivable

| Type | Description | Advance Rate | Fees | Best For |

| Factoring | Sell invoices to a third party | 70–95% | 1–5% per month | SMEs, exporters |

| Invoice Discounting | Borrow against invoices | 80–90% | 0.5–3% monthly | Established firms |

| Spot Factoring | Finance single invoices | 70–90% | 2–6% | Seasonal businesses |

| Recourse Factoring | Business bears risk | 80–95% | Lower fees | Strong customer base |

| Non-Recourse Factoring | Factor bears risk | 70–90% | Higher fees | Risk mitigation |

Classification

Said accounts qualify in the financial statements according to their origin in:

- Commercial: The income produces from goods and services corresponding to the business’s primary operations.

- Affiliates: product of transactions made with relatives and related companies.

- To employees: From loans, advances, or other deliveries given to workers and that they return in a given time.

- Other accounts receivable: Those that come out of the company’s regular operations.

The Accounts Receivable Financing Process

- Generate Invoice: Your customer orders a product and issues a purchase order or contract. You proceed to generate a bill of sale.

- Submit Invoice: Instead of waiting 30-45 days for payment, you choose to submit your invoice to RTS International.

- Receive funds: RTS International advances you a percentage of the invoice and retains a balance in reserve.

- Collection management: RTS International collects the entire invoice from its client.

- Complete process: RTS International credits the balance held in reserve less a modest charge for assuming collection risk.

Benefits of Accounts Receivable Financing

- Funds can be transferres the same day the bill is deducte.

- The service package includes collection management and internal support services (back-office).

- Credit evaluation services include helping you assess the creditworthiness of your clients.

- Accounts receivable financing is corrupt on the creditworthiness of your customers, not the financial results of your business.

- Accounts receivable financing is not a loan and does not appear as a debt on your balance sheet.

Accounts Receivable Financing vs Other Funding Options

| Feature | AR Financing | Bank Loan | Line of Credit |

| Approval Speed | Fast | Slow | Medium |

| Collateral | No | Yes | Sometimes |

| Flexibility | High | Low | Medium |

| Cost | Medium-High | Low | Medium |

How is Accounts Receivable Financing Used?

- Accounts receivable financing can help your business raise. By getting paid faster, you’ll be able to relieve the pressures of payroll obligations, qualify for additional financing options, access early payment discounts, and much more.

- Accounts receivable financing usage by companies whose customers take 30-60 days or more to pay their invoices; using funds receivable financing, your business will receive payments much faster.

- Companies with rapid growth and high demand for short-term working capital use accounts receivable financing to support their growth.

- Companies with large fluctuations in sales use accounts receivable financing to stabilize their cash flow.

Country-Wise Providers & Pricing Table

| Country | Provider | Advance Rate | Fees | Resource |

| USA | BlueVine | 85–90% | 1–3% | https://www.bluevine.com |

| USA | Fundbox | 70–90% | 2–5% | https://fundbox.com |

| India | Drip Capital | 80–90% | 0.5–2% | https://dripcapital.com |

| India | KredX | 80–95% | 1–2% | https://kredx.com |

| UK | MarketFinance | 85–90% | 1–4% | https://marketfinance.com |

| Australia | Octet | 75–85% | 1–3% | https://octet.com |

| Canada | FundThrough | 80–90% | 2–4% |

How can I get my Clients to Pay on Time?

Achieving an effective and healthy collection process in the company is a challenging task that requires attention and preventive actions; it will always be easier to collect a current account than an expired one; to achieve more efficient management.

- The preventive collection consists of notifying the client days in advance that he has an invoice that is about to expire to schedule its payment and avoid having an overdue account.

- Discounts for early payment: An incentive that a seller grants to a buyer for payments made before the scheduled maturity of the debts incurred.

- Automation of payment reminders: Through a technological tool, you can generate reminders for your customers about the due date before it occurs to include it in their payment planning.

Competitor Comparison Table (Top Platforms)

| Platform | Approval Time | Advance Rate | Fees | Unique Feature |

| BlueVine | 24 hrs | Up to 90% | Low | Fast funding |

| Fundbox | Minutes | 70–90% | Medium | AI credit model |

| Drip Capital | 2–5 days | 80–90% | Low | Export focus |

| KredX | 48 hrs | 80–95% | Low | Marketplace lending |

| MarketFinance | 24–72 hrs | 85–90% | Medium | Flexible contracts |

Industry-Wise Use Cases

| Industry | Use Case |

| Manufacturing | Purchase raw materials |

| Export/Import | Bridge international payment delays |

| Logistics | Cover fuel and operational costs |

| Staffing Agencies | Payroll funding |

| Wholesale | Inventory restocking |

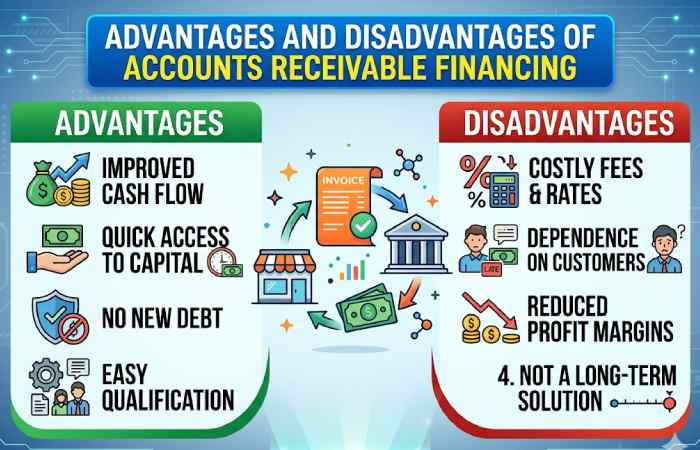

Advantages and Disadvantages

Accounts receivable financing allows businesses to have instant access to cash without dealing and struggling with the long waits associated with obtaining a business loan. In addition, when a company uses its accounts receivable to sell assets, the problem does not have to worry about payment terms when a company sells its versions receivable.

It does not have to worry about collecting them. When a business receives a factoring loan, the problem can immediately get 100% of the value.

Although accounts receivable financing offers several advantages, it can also negatively affect. In particular, receivables financing can cost more than funding through traditional lenders, especially for businesses that have poor credit. In addition, companies can lose money from the margin paid on accounts receivable in an asset sale. Finally, the interest expense can be high with a loan structure or much more than discounts or charge-offs.

Future Trends (2026 & Beyond)

- AI-driven credit underwriting

- Blockchain-based invoice verification

- Embedded finance in ERP systems

- Growth of cross-border financing platforms

- Integration with accounting tools like QuickBooks

When Should You Use Accounts Receivable Financing?

Rapid growth phase

Cash flow gaps

Seasonal demand spikes

Export-heavy business

Limited access to bank loans

Conclusion

Accounts receivable financing has become a better alternative to traditional finance for businesses that cannot obtain loans. In today’s economy, you need to keep your customers happy while covering all your expenses. As a result, some business owners will rely on credit cards and business loans to cover their costs.